Sunday - Day 7

So, it's Sunday and the end of week 1 of the All You Grocery Challenge. Today we had a late breakfast of pancakes, eggs and toast, and milk. For lunch we had turkey sandwiches, made with the turkey and rolls that were given to us, a slice of watermelon each and chocolate milk. For dinner I plan on making Chicken and Biscuits (the kind I make has mixed vegetables in it), fruit for dessert (choice of strawberries, blueberries, or grapes) and juice (100% fruit juice) for our drinks.

A Week in Review

Well, we made it through the first week under budget. We would have spent a lot less but life got in the way. With the water being turned off on Wednesday, we ended up spending $20 on a sheet pizza. Then on Friday, my husband and I celebrated our anniversary. We ended up going to Olive Garden and spending $38.02. If you subtracted just those two things, we would have spent almost $60 less. Isn't it crazy how much you can spend just eating out?

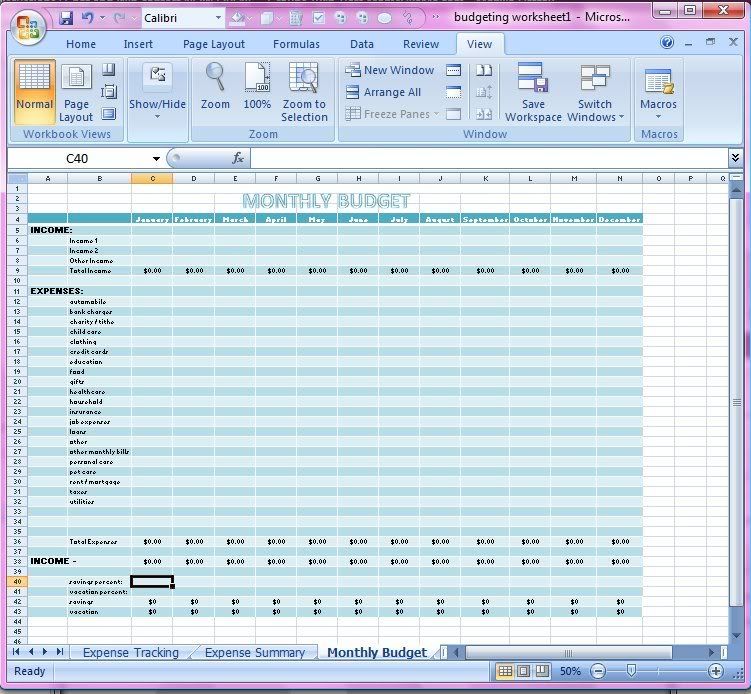

Here is what my spending log I use looks like. I used all those wonderful skills I learned in my Advanced Spreadsheets class. You can click on it to take you to a larger picture of it.

I track each day's spending on food for each week. I also have a drop-down menu to use for my category - they are sorted by food, eating out and snacks/coffee. I then added each category up and did a nice pie chart to help me see where I am spending my food money.

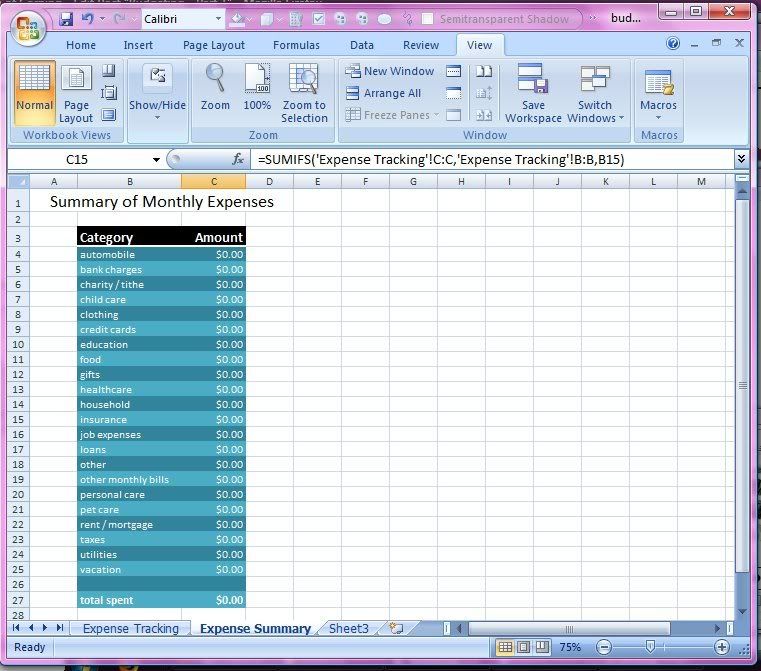

I did a screen shot so that you can see how much I spent this week. Here is Week 1's Totals and chart. You can also click on the this picture in order to get a bigger picture.

As you can see in the above chart, I spent $67.90 on eating out (pizza and anniversary), $4.23 on snacks and coffee, and $20.38 on groceries. We still have $32.49 out of our allotted $125 budget for the week. The pie chart shows all $125 of our food budget, blue is eating out, red is snacks and coffee, green is groceries and purple is what we have leftover.

So, we did pretty good, all things considered. Next week will only be better. My local grocery store does have a few good deals so we will be stopping there sometime during the week.

I did a screen shot so that you can see how much I spent this week. Here is Week 1's Totals and chart. You can also click on the this picture in order to get a bigger picture.

As you can see in the above chart, I spent $67.90 on eating out (pizza and anniversary), $4.23 on snacks and coffee, and $20.38 on groceries. We still have $32.49 out of our allotted $125 budget for the week. The pie chart shows all $125 of our food budget, blue is eating out, red is snacks and coffee, green is groceries and purple is what we have leftover.

So, we did pretty good, all things considered. Next week will only be better. My local grocery store does have a few good deals so we will be stopping there sometime during the week.

{kind=link}